Award-winning PDF software

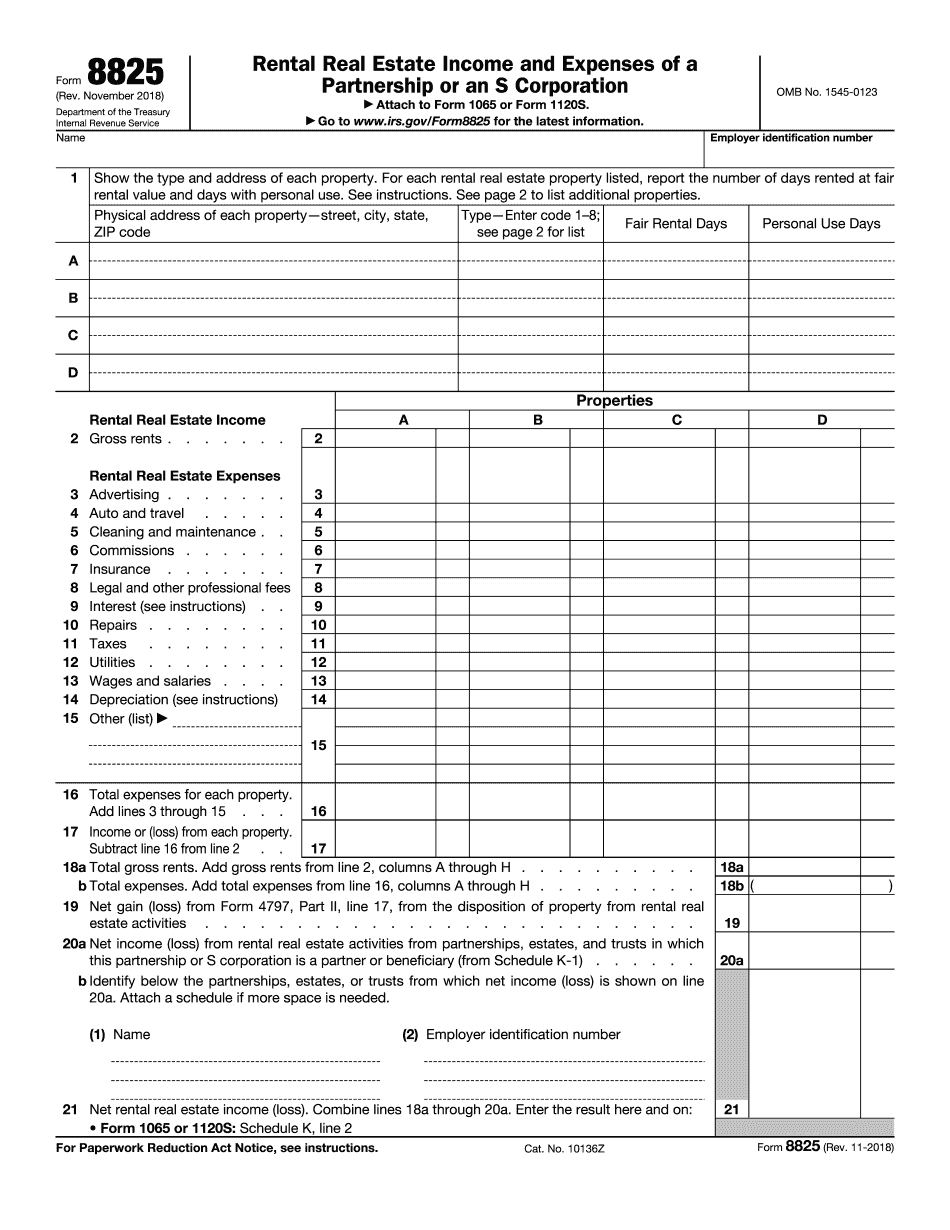

Form 8825 for Detroit Michigan: What You Should Know

Expensing— Michigan Department of Treasury “Effective January 1, 2015, a taxpayer may deduct the capital cost of property, qualified improvements on the property, including depreciation, and other expenses incurred since January 1, 2000.” “In general, when there are items of property to be depreciated, the property is depreciable in full, and when there are expenses incurred for property not yet fully depreciated, the deduction may not be allowed (even if the depreciable portion is determined to be capital).” Expensing Expenses Not Determined By Income — Michigan Dept. Of Treasury (MI FOR) “The expense of buying or making land, as well as property acquired as a result of real estate taxes, is not considered capital expenses if the land or property has not been used for any business except farming. However, if land had been previously used for farming, the owner may not subtract depreciation amounts on that land.” “If your farm's property was used for business before being deemed qualified, then you can deduct its cost in full under Section 179 for business use. If your farm property was never used for any business at all, then you may not deduct its cost in full under Section 179 and instead will be charged certain ordinary and necessary expenses which are limited in the maximum amount of the deduction (see Publication 450).” In other words, if you have owned a piece of land for a year, you can deduct all you paid for it plus expenses for that year. If it was never sold you can deduct some or all the cost you paid. “If you sold land to raise farm production or a share of the profit from farm production over a one-year period and there was a loss, then the amount of the depreciable gain or loss cannot exceed that of your property. The gain or loss from real or personal property used and owned by you for farming business purposes cannot exceed the maximum amount of depreciation allowed for farm real property.” “If you had an item of capital property that was a farm business asset, and you lost this asset, and it could have been used for farming business purposes, you can deduct a loss from the sale of it, provided you sell it within two years after the sale.” This can help offset the real estate tax you paid on the asset.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8825 for Detroit Michigan, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8825 for Detroit Michigan?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8825 for Detroit Michigan aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8825 for Detroit Michigan from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.